Economy

Bitcoin Un-Tethered

The market decides what it wants not you or me.

Did you happen to notice the big news in Bitcoin the other day? It wasn’t the sound of the top forming at $59,000 or Janet Yellen’s comments about its ‘inefficiency.’

It was settling, once and for all, the argument that central planners and oligarchs aren’t omnipotent.

The State of New York’s pathetic slap on the wrist of Tether marked the moment Bitcoin joined the ranks of the ‘Too Big to Fail.’

Somewhere Peter Schiff is sad.

This lawsuit was supposed to be the nuclear bomb goldbugs thought would finally blow up bitcoin and return the world to their vision.

Too bad that multi-megaton nuke was more like an M-80 going off in my neighbor’s backyard.

“Tether’s claims that its virtual currency was fully backed by U.S. dollars at all times was a lie,” James said in a statement. “Bitfinex and Tether recklessly and unlawfully covered-up massive financial losses to keep their scheme going and protect their bottom lines,” she further said, adding: “These companies obscured the true risk investors faced and were operated by unlicensed and unregulated individuals and entities dealing in the darkest corners of the financial system.”

This is a face-saving statement for the press by NY Attorney General Laetitia James. Because if there really was a Ponzi scheme at the heart of Tether’s business in 2018-19 then she would have gotten them to cough up a helluva lot more than $18.5 million.

If the powers that be could destroy bitcoin at this point they would have pressed further charges against Tether, undermining the structure of the entire bitcoin market which is increasingly becoming a function of Tether liquidity.

But they didn’t.

In fact they gave Tether and Bitfinex the same treatment they gave J.P. Morgan for gold and silver market manipulation and the entire mortgage industry for fraudulently robosigning legal documents.

In other words, ‘We fined some folks.’

Most, if not all of the anti-bitcoin arguments come down to “the government hates it they will ban it.” But what happens when the government admits it can’t?

So while, Murray Rothbard was right, the establishment hates a free market more than anything else, Murray was also right that their is a limit to their power.

Um, someone tell Janet Yellen and Bill Gates running the anti-environment talking point that Bitcoin uses a lot of electricity isn’t working.

It’s the oligarchs’ latest talking point. And it’s pathetic.

Someone tell Laetitia James to get back in there and fight.

Meanwhile Bitfinex and Tether agree to quarterly monitoring of their books as a gesture of “transparency” and add $18.5 million to the failing tax coffers of New York State.

Whatever hinckey stuff they do they will now — like the major primary dealer banks — settle up at the end of the quarter to present the face to meet the regulators that they meet (with apologies to T.S. Eliot).

And, make no mistake, I think Bitfinex and Tether are sketchy as all get out. In fact, I think 95% of the entire crypto market is sketchy.

But, that doesn’t make it unreal or becoming something unstoppable. Because it doesn’t matter what purists want. The market, in the aggregate, is smarter than any one person.

And the market wants what bitcoin and Tether are selling… right now.

It may want something different in the future. The market is nothing if not fickle…. and gods bless it for this.

Which brings me to why this lawsuit is so important. There was a recent uptick in anti-tether noise out there, doomsdaying the latest bitcoin rally.

This article “The Bit Short: Inside Crypto’s Doomsday Machine“ (very long, and reasonably well researched) from January outlines a strong argument as to why Tether could be a scam.

And I want to point out how well-timed it was, published January 14th, coinciding with the first attempt to derail bitcoin’s rise.

He goes into a lot about Tether, staking his entire argument on their responding to this lawsuit as the proximate cause for their cashing out of their scam.

He does a forensic analysis of the Bahamanian banking system, lays out the mechanisms for startup company scam, the whole nine yards. Kudos to the writer, it’s a good tale you should read it.

He also didn’t sign his work, but, you know, details.

That doesn’t mean however:

- He’s right.

- Things can’t evolve or change.

- Tether isn’t performing a valuable service

- Demand for bitcoin liquidity outstrips available supply

In the end, this is just another great piece of writing that misses the bigger picture.

The market decides what it wants not you or me.

In short, it doesn’t mean Tether was intended to be a scam but could simply have been, like bitcoin itself, a service so needed by the market that demand for it far outstripped its ability to perform within its operating parameters, i.e. 100% dollar reserves 100% of the time.

That’s the main reason why Laetitia James settled out of court and Tether admitted no wrongdoing. The market was simply moving faster than the money pouring in and out of the crypto-space could clear and they shuffled some money around to, in the end, protect their clients and their business.

Here’s an aphorism which bears on this story, “It’s easier to beg for forgiveness than permission.”

$18.5 million and a negative headline is cheap to protect what is now a $35 billion business.

But, the premise of this article has been a standard refrain in the crypto-skeptic land for four years.

It boils down to, “You all know Tether’s a scam, right!?”

It’s a glaring bit of editorial bias. Because many of the arguments that people make about bitcoin and cryptocurrencies in general are built on the premise that everyone holding them wants to at some point “cash out and get back to dollars.”

But what does the market look like when a critical mass of people make a psychological shift valuing their portfolios not in dollars but bitcoin?

One could argue we’re in the process of finding out the answer to that right now.

I’ve talked about the potential for this shift previously here, here and here for anyone who still isn’t listening.

And that scares the living daylights out of everyone who makes their money outside of the dollar, bull or bear, but especially the bears.

Because for a generation now those bears were sold by people like Peter Schiff and the writer of this article which was disseminated far and wide in gold circles that gold was the only alternative to the dollar.

But it’s not and they are bitter about it.

They created what I now call “Gold-Only Bugs.”

For four years I’ve listened patiently to every argument against bitcoin and tether. They aren’t completely wrong. But they do, I think, overstate the risks.

I continue to hedge my bets against monetary insanity. I’m one of the few people in this space that advocates de-risking across all cash-equivalent asset classes.

With this lawsuit and the whole Tether Time Bomb removed from the market bitcoin is now part of the big time. It’s a multi-trillion industry. Those don’t just dry up and blow away without damaging the very people trying to defend against it.

When you owe the bank a thousand dollars it’s your problem. When you owe the bank a trillion dollars it’s their problem Bitcoin is a variation on that idea.

Blackrock’s buying bitcoin, folks.

Blackrock.

Coinbase is filing for an IPO. It’ll be at a valuation higher than Facebook’s.

In fact, it’ll be the biggest IPO in U.S. market history.

The bookrunning fees alone will make Goldman’s or Morgan’s next quarter a blowout.

They said the internet was a fad, too.

But yet you still think a troika of Participatory Medal Winners like Janet Yellen, Christine Lagarde and Jerome Powell are going to stop this train?

You think they can just wave their magic wands and make it all go poofta?

Why would Tether and Bitfinex run away with all the money now when they just won? Bigly.

They can pull massive yield in DeFi on their USDT and bitcoin. But they’re going to give up their first-mover advantage in the immensely important stablecoin space for a couple of billion which can be seized by any government?

The only central banker with a brain is Powell, as he properly identified the threat to their rule… and it’s not bitcoin.

It’s stablecoins like tether.

Because what is the dollar except a stablecoin backed by the confidence of the debtholders of Nancy Pelosi’s ability to extract wealth from Americans to pay the coupons?

If someone builds a better one than the dollar eventually it’s game over for the debt-based system.

Why would Tether run away with a few billion in depreciating dollars when they can literally bring down the entire monetary system and replace it with their product?

The reality is that the day the dollar becomes irrelevant is the day Tether folds up shop and completes their scam because no one will want dollars and a dollar-pegged stablecoin with dollar reserves will be redundant.

I’m not saying that day is here. No. We’re a long way off from that day.

But this lawsuit settling with such a whimper is a primal scream marking the next phase of the war between central banks and the people.

Economy

McMaken: The Fed’s Inflation Is Behind the Supply-Chain Mess

… the idea that supply chain problems are “driving inflation” gets the causation backward.

It seems supporters of the Biden Administration finally settled on a narrative they like for explaining away supply chain shortages.

Here’s the administration’s talking point: the US economy is rolling along so well that Americans are demanding huge amounts of goods. That’s overwhelming the supply chain and causing the back-ups roiling America’s ports and logistic infrastructure.

For example, Transportation Secretary Buttigieg this month declared “Demand is up … because income is up, because the president has successfully guided this economy out of the teeth of a terrifying recession.”

Similarly, White House spokeswoman Jen Psaki told reporters supply chain problems are occurring because “people have more money … their wages are up…“we’ve seen an economic recovery that is underway…”

This position has been mocked by a number of conservative politicians—including Senator Ted Cruz—and commentators who find this to be an absurd assumption.

Yet, the administrator’s defenders aren’t totally wrong. As Mihai Macovei showed earlier this month, the global volume of trade and shipping volume in 2021 have actually exceeded pre-pandemic numbers. For example, in the port of Los Angeles, “loaded imports” and “total imports” for the 2020-2021 fiscal year (ending June 30, 2021) were both up when compared to the same period of the 2018-2019 fiscal year.

In other words, it’s not as if nothing’s moving through these ports. In fact, more is moving through them than ever before. That suggests demand is indeed higher.

But why is it higher? It some ways, it’s true that, as Psaki says, people have more money.

But that’s where the veracity and usefulness of Biden’s defenders end in explaining the problem.

Much of the answer can be found in monetary inflation. Obviously, Joe Biden hasn’t “successfully guided the economy” through anything, but it is accurate to say that people have more money in a nominal sense. Wages are up nominally. After all, if we look at the immense amount of new money created over the past 18 months, we should absolutely expect people to have more money sloshing around. But this also means a lot more pressure on the logistical infrastructure as people buy up more consumer goods.

In other words, the idea that supply chain problems are “driving inflation” gets the causation backward. It’s money-supply inflation that’s causing much of the supply chain’s problems. Not the other way around.

After all, since February 2020, M2 has increased from $15.2 trillion to $20.9 trillion in September 2021. That’s an increase of 35 percent. Yes, some of that has been kept within the banking system through the Fed’s payment of interest on reserves, but a lot of it clearly has entered the “real economy” through stimulus payments, unemployment insurance, and federal deficit spending in general.

Originally, the public was saving a lot of that stimulus and bailout money, with the personal savings rate hitting historic highs of over 25 percent. But this past summer the savings rate collapsed again, and as of September is back under eight percent. The public is now flooding the economy with its former savings.

The American appetite for spending on consumer goods hasn’t gone away. Yet, there are many reasons to suspect this spending spree is unsupported by actual economic activity, and in a phenomenon of monetary inflation.

For example, today’s tsunami of spending raises questions when we consider there are still about five million fewer people working in the American economy than was the case in early 2020. That means fewer people being paid wages. Without monetary inflation, an economy with millions of fewer workers suggests there should be less spending.

Additionally, spending increases when the public suspects that inflation is going to increase. That is, if there is perception the value of money will decline, the demand for money will decline also. As Ludwig von Mises noted: “once public opinion is convinced … the prices of all commodities and services will not cease to rise, everybody becomes eager to buy as much as possible and to restrict his cash holding to a minimum size.”

That means more spending. This phenomenon is already clear in home prices and grocery prices. The public may suspect rising prices are here to stay. Meanwhile, the Consumer Price Index—a very limited measure of goods-price inflation—is nonetheless near a 35-year high. That means now’s a good time to spend.

With 2020’s panic-induced saving subsiding, people are now wondering if their savings produce any returns. But ordinary savers are surely now remembering that the interest returns from savings right now are next to nothing. Thanks to the central bank’s ultra-low interest rate policy, we live in a yield-starved world. That’s OK for hedge funders who can participate in carry trades and other high-yield forms of investment. But for regular people they’re stuck with interest rates that don’t keep up with price inflation. So it makes more sense to spend dollars rather than save them.

So, Biden’s people are correct in a certain sense that people have “more money” and that “demand is up.” With federal spending hitting historic highs—and half of it is deficit spending that’s being monetized—we should expect people to have “more money.” This is just what we would expect in an inflationary environment. We should expect demand for everything (but money) to be up.

The question, however, is how much of this windfall will continue in real, inflation-adjusted terms. It’s too early to tell, although we can also see that inflation-adjusted median earnings collapsed 6.3 percent, year over year, during the second quarter of 2021. We can see that real GDP growth has dramatically slowed.

But at least as far as the third quarter is concerned, it’s fairly clear the US was—and likely still is—in the midst of an inflationary boom. But how long will it last?

Economy

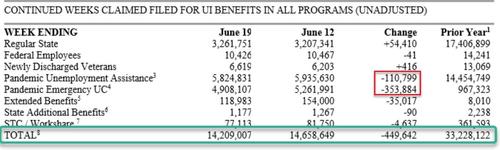

There Are Still Over 14 Million Americans On Some Form Of Government Dole

… we remind readers of the gaping chasm between those still claiming some form of pandemic-related unemployment benefit and the record number of job openings in America currently…

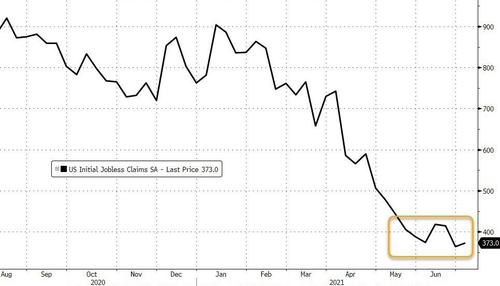

Initial jobless claims hovered at post-COVID-lockdown lows but were disappointing at 373k – well above the 200k-ish norms of pre-COVID

{kind=link}

Source: Bloomberg

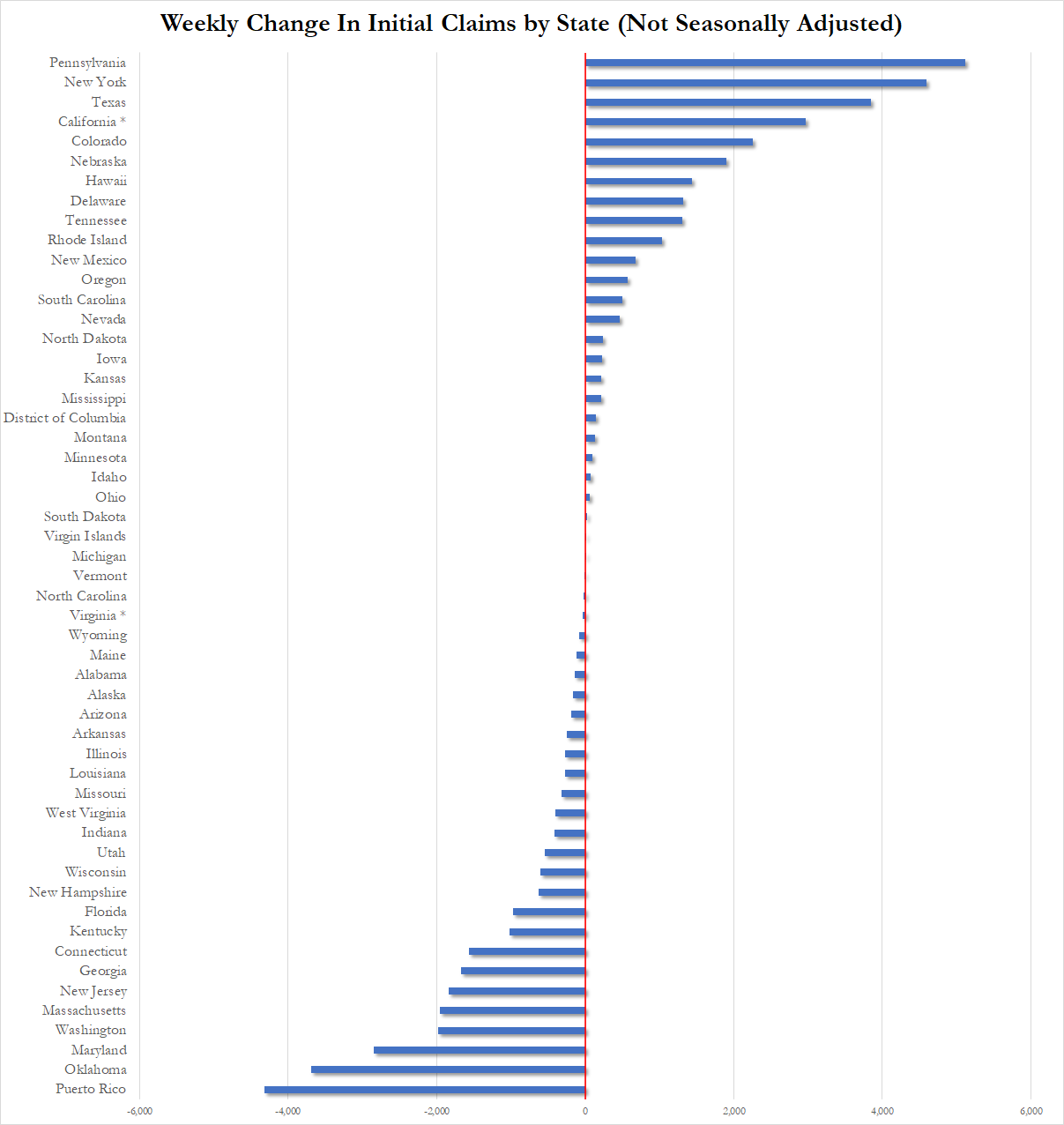

Notably, California and Virginia ‘estimated’ their jobless claims last week and Pennsylvania continues to swing wildly from week to week…

{kind=link}

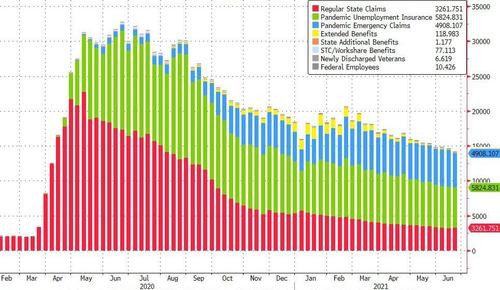

But, while the picture is improving overall, we should still remember that there are over 14 million Americans still on some of government dole…

{kind=link}

Source: Bloomberg

We do note that 460k Americans dropped off the pandemic emergency aid rolls…

{kind=link}

Finally, we remind readers of the gaping chasm between those still claiming some form of pandemic-related unemployment benefit and the record number of job openings in America currently…

{kind=link}

Source: Bloomberg

Tick-tock on those benefits.

Economy

The Fed in a Box Part 2: They Cannot End Quantitative Easing

If inflation doesn’t slow in the coming months, the Fed may be forced to step in.

- If the Fed tapers QE, it may reveal waning appetite for long-term treasuries

- The Treasury may have used its cash balance reserve to anchor inflation expectations

- If inflation persists, the Fed may have to increase rather than decrease QE

Note: By definition, inflation is an expansion of the money supply. In this article, inflation will be used interchangeably with rising prices (usually as a result of money supply expansion)

Introduction

When the economy was shut down in March 2020, the government responded with massive fiscal and monetary support. The fiscal stimulus totaled $4T+ in relief packages. All of this spending was paid for with debt issued by the Treasury. The Treasury mostly issued short-term debt. With rates being held at zero by the Fed, and strong demand for short-term debt, it made sense to quickly raise cash using Treasury Bills as interest-free loans.

The Fed monetary policy was two fold, slash short-term rates to zero and inject $1.5 trillion into the long-term debt treasury market. The effect was to bring down interest rates across the entire yield curve. After the initial debt binge, QE went on auto-pilot, with the central bank buying about $80B a month in long-term debt (plus another $40B in Mortgage debt). Over the last year, the Treasury has continued to issue long-term debt, averaging more than the $80B the Fed has been buying. This has caused long-term rates to rise.

All of this fiscal and monetary stimulus is not without cost. Historically this type of activity almost always leads to higher inflation. The Fed may have recently indicated it wants higher inflation, but this is not true. This stance simply provides cover for them to not act in the face of rising prices. To actually fight inflation, the Fed would have to increase short-term rates above the rate of inflation. Part 1 of this series went into detail about how US short-term debt has doubled from $2.5T to $4.5T. This makes even small changes in short-term rates an immediate risk to the federal government, not to mention the much higher rates needed in a true inflation fight.

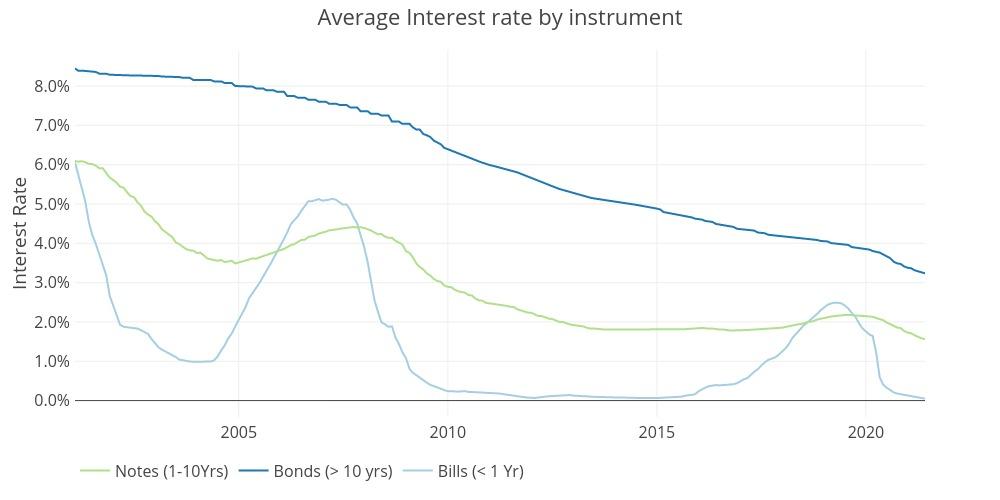

In theory, the Fed could leave short-term rates at 0% while ending QE and even shrinking its balance sheet. This would push long-term rates up to combat inflation. In the short/medium term the Treasury can mathematically handle higher long-term rates because it takes time for the higher rates to work their way through long-term debt. See the chart below that shows how the last tightening cycle worked its way through the average interest rate across debt instrument. Specifically, look at Notes compared to Bills. The average weighted interest rate on Bills moved very quickly where the rate on Notes barely had time to increase before rates dropped again.

Source – Treasurydirect.gov

Although the Treasury could handle rising long-term rates (even if the economy and mortgage market cannot), the Fed has another problem. Rising long-term rates send an important message: rising inflation expectations. While inflation is first and foremost a result of monetary policy, higher inflation expectations quickly exacerbate the problem. This is why the Fed has been messaging they are OK with higher inflation and also why they have been pounding the table that inflation is transitory. They need to keep inflation expectations low! If inflation expectations were to rise, especially at this critical juncture, it would be game over for the Fed, as they would have to raise short-term rates (devastating the Treasury and economy) in order to save the dollar and squash inflation.

With the economy opening up in March of this year, things were getting very precarious as inflation was rapidly rising along with surging long-term rates. Remember that rising long-term rates indicate rising inflation expectations. This could cause transitory inflation to be much less transitory.

In summer 2020, the Treasury issued enough debt to build up a significant cash reserve. In response to rising long-term rates in Q1 2021, it appears the Treasury strategically used its cash reserves to slow down the issuance of long-term debt. With total short-term debt outstanding already so high, the cash balance gave the Treasury ammunition to decrease debt issuance just as a $1.9T stimulus bill was passed and inflation was set to explode higher. This would have been perfect timing to support the Feds narrative that inflation is transitory to keep expectations from snowballing out of control.

If inflation doesn’t slow in the coming months, the Fed may be forced to step in. With the Treasury poised to issue more debt, it can no longer rely on its one-time use of excess cash reserves. This will put more pressure on the Fed to clamp down long-term rates by increasing rather than decreasing QE. Yes, the Fed may decide to print more money (leading to higher prices) to fight rising inflation expectations (higher long-term interest rates).

Understanding recent fiscal and monetary maneuvers

Last year, when the pandemic hit, the US Government started spending trillions of dollars. Massive spending plans were approved in the name of stimulus and COVID relief. Because the government does not have much money on hand, and taxes cannot quickly be raised, the Treasury issued trillions in debt. The markets can easily absorb short-term US Treasury Bills, so when the Fed abruptly cut rates to 0%, the Treasury responded by issuing short-term debt to the tune of $2.4T from March to June 2020. See figure 1 below.

Source – Treasurydirect.gov

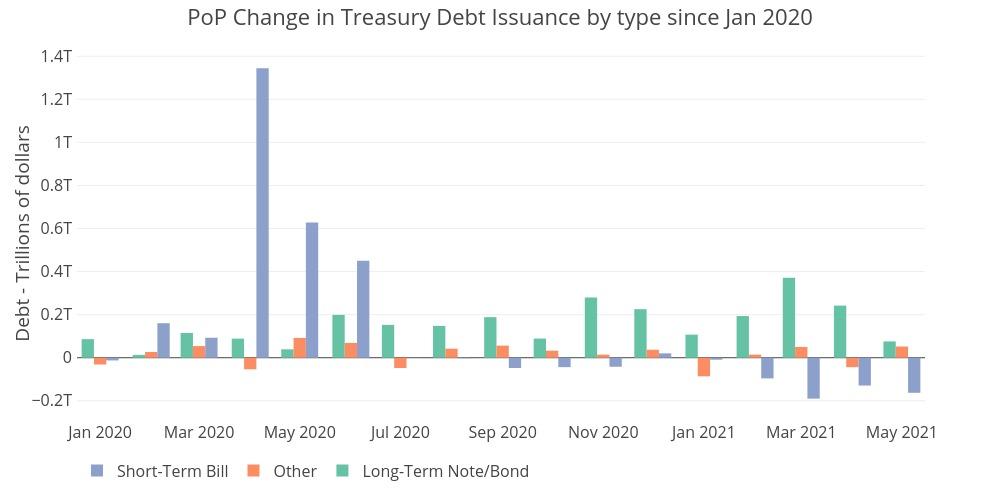

In tandem, the Fed bought up trillions of dollars in US Debt, but the Fed was buying on the long end of the curve while the Treasury was issuing debt on the short end. This caused long-term rates to collapse. The Fed purchased enough long-term debt to absorb more than a year’s worth of long-term debt issuance. The chart below shows how the month over month and cumulative change in the Feds balance sheet compared to the Treasury Debt Issuance of long-term notes and bonds.

Source – Treasurydirect.gov

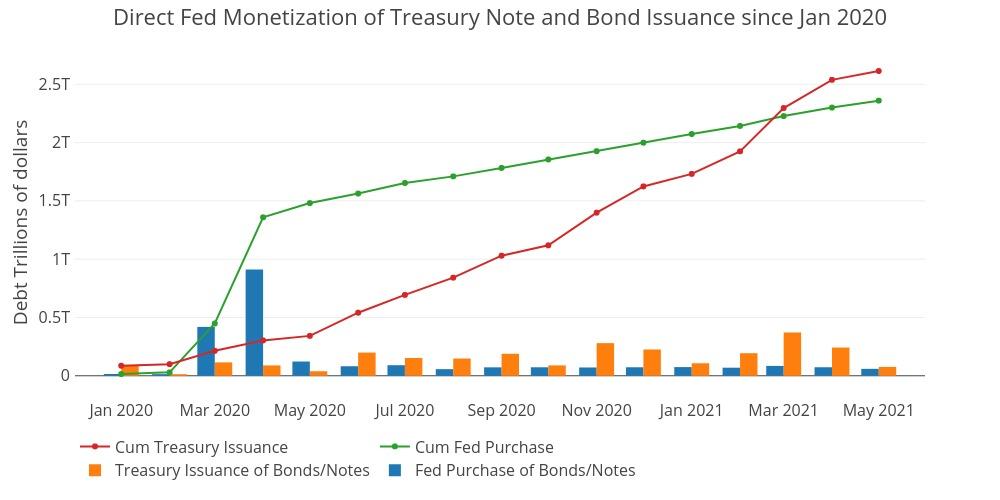

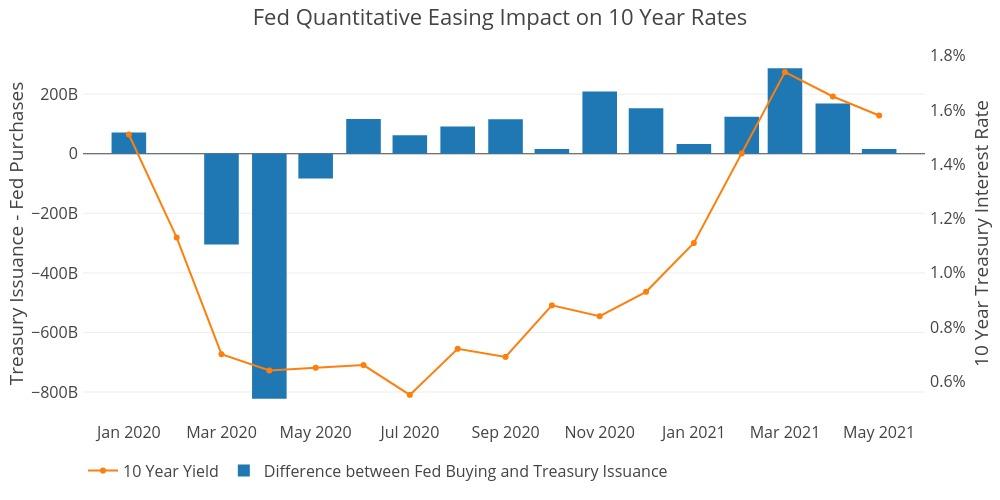

This action by the Fed had a massive impact on long-term rates. The chart below shows the difference between the two bars above, specifically the difference in Fed Buying and Treasury issuance of long-term debt for each individual month since Jan 2020. These values are not cumulative. The right Y-Axis shows the month-end interest rate of the 10-year bond. Looking at this chart shows something extremely clear: When the Fed buying exceeds debt issuance, rates are flat or falling; however when long-term debt issuance surpasses the Fed’s buying, rates rise.

Source – Treasurydirect.gov

The impact of the Fed can first be seen as interest rates fell from 1.5% to .6% during the initial buying spree. After the initial burst, the Fed put QE on auto-pilot, buying “only” $80B a month in long-term Treasuries. However, because the Treasury was issuing more than $80B a month as depicted by the positive bars starting in June 2020, interest rates started rising.

This trend started to accelerate in November of 2020, as long-term debt issuance was outpacing Fed Buying by around $200B. Things really started to escalate in the first quarter of 2021 as Treasury Debt issuance surpassed Fed buying by $286B in March right as interest rates were crossing above 1.7%.

Then, suddenly, long-term debt issuance started falling in April and was almost even with Fed buying in May. This consequently led to a fall in long-term rates, which are now hovering back around 1.5%. How did this happen just as Biden was pushing through a $1.9 stimulus package? Unlike 2020, when short-term debt issuance was used to plug the gap, Figure 1 above shows that short-term debt issuance was actually turning negative (blue bars).

What gives?

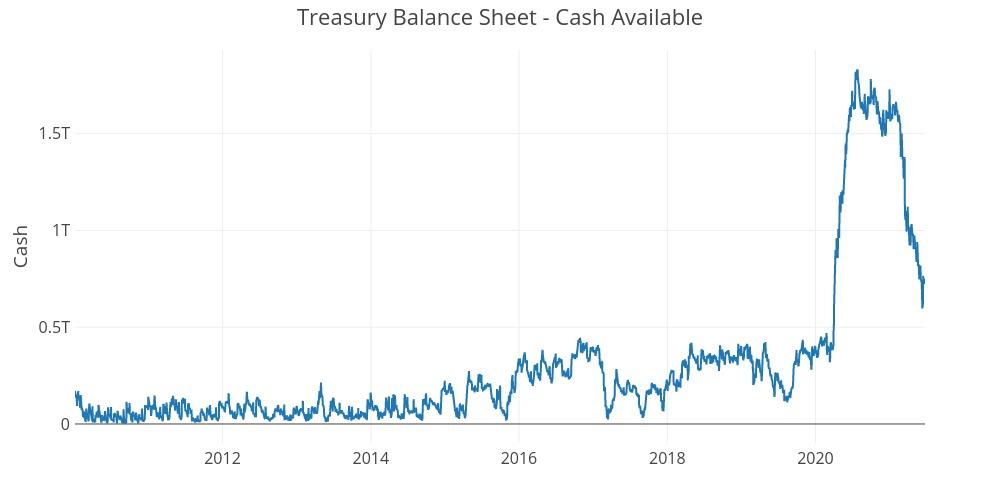

One look at the Treasury Cash Balance sheet in the chart below tells almost the entire story. This was first highlighted by a SchiffGold article published June 16. The chart below shows a massive surge in cash reserves by the treasury last year. Since March of this year, the cash balance has plummeted by over $1T.

Source – Treasurydirect.gov

Inflation Expectations

Why such a massive and sudden drawdown in the cash balance? In truth, there could be lots of reasons, but it does seem extremely sudden. One would think the Treasury, led by Yellen, would be very deliberate and thoughtful about how to use up $1T+ in dry powder. For the past 3 months, the Fed has been shouting from the rooftops that inflation is transitory. At the June FOMC press conference, Powell stood up and explained how long-term inflation expectations remain well-anchored. A proxy for inflation expectations is long-term interest rates.

Had interest rates continued to rise similar to the recent trajectory (climbing from .8% in Nov to 1.7% in March), this would have been a difficult narrative to push. The Fed needs inflation expectations to remain in check or else inflation will be anything but transitory. Thus, the perfect time for the Treasury to pause issuance of long-term debt would be April-June 2021 just as the economy is re-opening and the Fed is forecasting inflation to be at its worst before coming back down.

While this is speculation, it would be a very strategic move from both Powell and Yellen. Regardless of the intention though, the problem is that the Treasury has now spent its large cash balance. It could return to the short-term debt market, but the outstanding balance is still sitting above $4T (see part 1). It needs to be converting that short-term debt to long-term debt while long-term interest rates are still low and the Fed is still buying. But the Fed is simply not buying enough at $80B to convert all that debt!

If inflation persists beyond a few months, then interest rates are going to rise in a hurry as the market demands higher rates. Adding fuel to the fire will be the Treasury debt issuance overwhelming the $80B Fed buying as it did from November to March.

Then what?

Who is absorbing the long-term debt to keep interest rates from returning to the upward trajectory from Aug 2020 – Mar 2021?

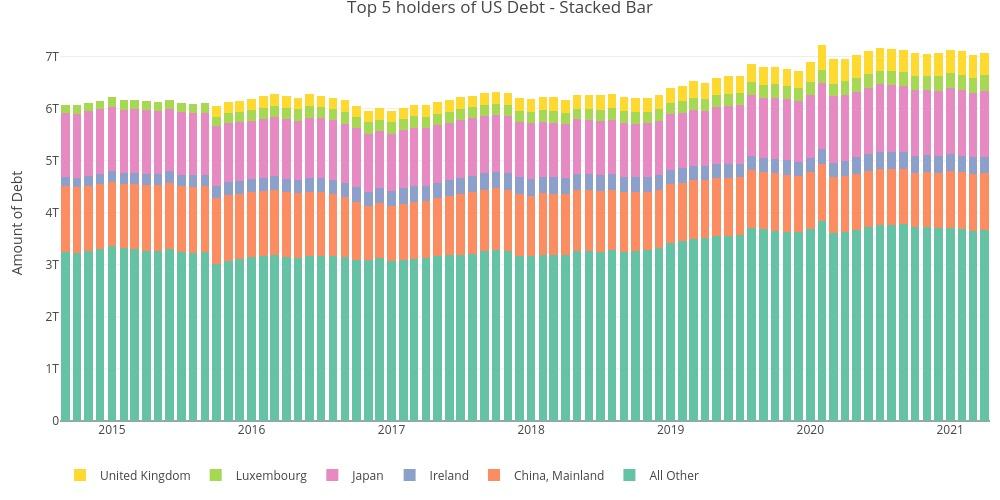

International creditors have had little appetite for US Debt lately. The chart below shows the total outstanding debt held by foreign governments. In the past 15 months, while the Treasury has issued over $4T in new debt, the net amount bought by foreign governments is close to zero.

Source – https://ticdata.treasury.gov/Publish/mfh.txt

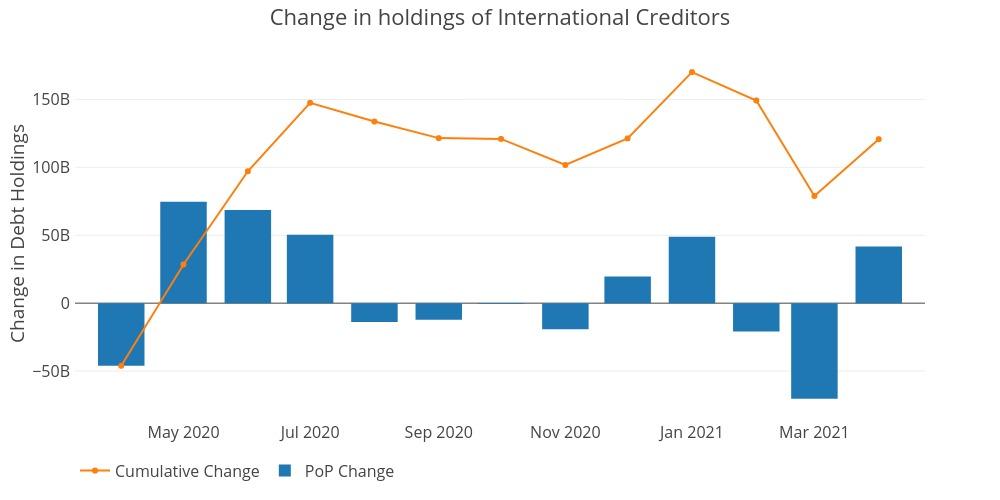

To zoom into the exact amount of change since the massive debt issuance, see the chart below. In total, foreign creditors have absorbed $120 billion of $6T+ or less than 2% of total issuance!

Source – https://ticdata.treasury.gov/Publish/mfh.txt

How are rates going to stay low if the Fed keeps the treasury buying cap at $80B? The Treasury will have to issue more than $80B in long-term debt to continue funding all the massive spending. If inflation expectations stay low, maybe the market will have enough firepower to ingest some of the new debt, but not all of it. With the Fed planning to begin tapering at the end of the year, someone will need to fill the $80 billion void. This does not even take into account the possibility of shrinking the Fed balance sheet, which should be considered impossible at this point.

The chart of the international holders above brings to mind the image of the Wiley Coyote running off a cliff. With 10-year interest rates hovering near 1.5%, one could argue there is strong demand for long-term Treasury debt. Unfortunately, foreign creditors have turned off their debt purchases. It took decades for them to accumulate ~$7T in Treasury debt. The Fed alone has accumulated more than half that (~$4.5T) over the last decade. The Fed is making the market seem strong, but as shown above, there might be nothing but air if they were to exit the market. With a thumb on the scale, no one is getting an accurate reading of true demand for US long-term debt.

Source – Warner Brothers

What about short-term debt markets?

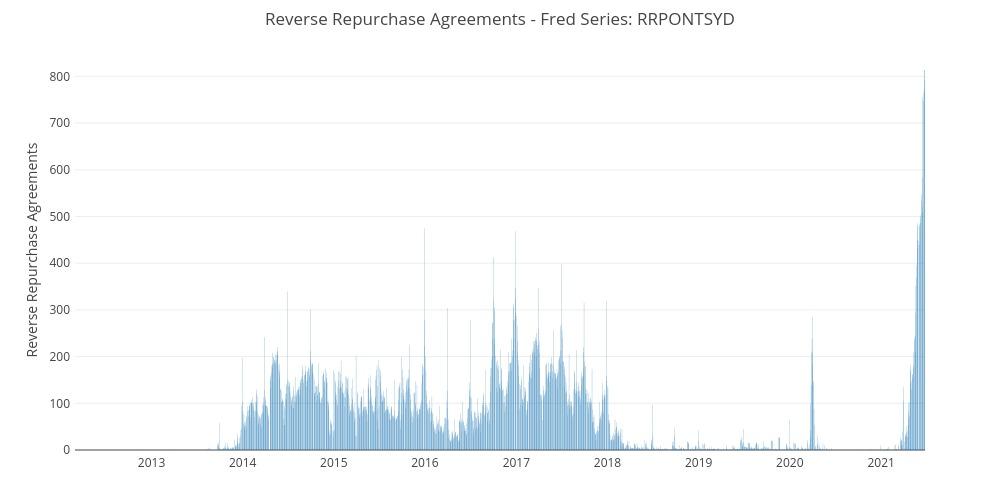

As highlighted several times, the demand for short-term debt seems to remain very strong. This makes sense as T-Bills mature in less than a year, so these investments are perceived as nearly risk-free. In fact, it could be argued that the recent Treasury Bill issuance hiatus (Figure 1 – blue bars turning negative) could be causing stress in the Reverse Repo market. The chart below shows the current Reverse Repo market. Based on past quarter-end data, it’s very possible that Reverse Repos could exceed $1.5T by this coming Wednesday, June 30, before coming back down.

Source – https://fred.stlouisfed.org/series/RRPONTSYD

Many articles have been written to explain this phenomenon, without providing exact clarity on what’s actually going on. The current understanding seems to be that the banks are awash with cash – so much cash, they are hitting the limits in terms of how much cash they can hold on balance overnight. This is cash that should be invested on behalf of money market funds. But with so much cash in the system, if it were to all be invested in short-term debt instruments, it could drive rates negative. To avoid negative rates, the Fed is lending banks assets on its balance sheet overnight in exchange for cash. It is critical to avoid negative rates to insure money market funds never experience a loss and result in breaking the buck.

Maybe this is a leap too far, but it seems another solution to the Fed reverse repurchase activity could be for the Treasury to issue more short-term debt. So, why has the Treasury been drawing down its cash balance and letting short-term debt mature when there seems to be strong demand in the market? The Treasury must recognize the risk of having too much debt in short-term instruments and is trying to lengthen the duration of its debt outstanding. Unfortunately, this abundance of cash in the repo market is in search of low-risk short-term debt so will not provide demand for long-term debt.

If this is the case, it has created quite the pickle for the Treasury. By issuing too much short-term debt, the Treasury is by default putting pressure on the Fed to not raise short-term interest rates. However, by issuing too much long-term debt, the Treasury is by default putting pressure on the Fed to maintain or even increase quantitative easing. To reiterate, this is why it is imperative the market believes inflation is transitory. The Treasury cannot stop issuing debt, which leaves the Fed unable to raise rates or taper QE without wreaking havoc in the bond market. Additionally, if the Fed has to fight inflation, then it’s not just the Treasury facing its Wiley Coyote moment, but the entire US economy.

Wrapping up

With the economy reopening, the Treasury deployed its cash balance at the most opportune time, unless of course inflation numbers continue to increase (which based on all the data, anecdotal evidence, and liquidity in the repo market seems like a strong possibility). Unfortunately for the Fed, the Treasury will have to begin re-issuing debt again. Will it lean towards short-term debt hoping the Fed keeps interest rates low, or long-term debt hoping the Fed will expand QE?

But Fed may be constrained either way because it has its own problem. Powell must be praying that inflation readings come in low AND job numbers disappoint. If both don’t occur, then tough questions will be asked to justify more stimulus. Yellen and Powell may be best buds, but simple coordination will not be enough. They will need magic and luck to keep the course steady heading into 2H 2021 and 2022.

If the Fed is lucky enough to get low inflation readings out of its rigged CPI, it may provide cover to begin tapering. Rising long-term rates won’t have the same compounding effect on inflation expectations in a “low” inflation environment. Unfortunately, long-term rates will not be tenable over the medium term as the government has to finance more and more debt. As the market this year has indicated, when issuance surpasses Fed buying, rates have gone up. So what happens to rates when the Fed leaves the market entirely? Presumably, they go up a lot. How high will the Fed let rates go before re-entering?

Just because something is inevitable (US Debt spiral) does not make it imminent; however, the next six months of data may shine a bright light on all the irresponsibility over the last 12 years if inflation proves not so transitory. Chances are, the only thing transitory will be “talking about talking about” tapering.

US Debt interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Join the community.

McMaken: The Fed’s Inflation Is Behind the Supply-Chain Mess

‘White People, You Are The Problem’: AT&T’s Internal ‘Racial Reeducation Program’ Leaked

Matrix? Misdirection? Cringe? Zuckerberg’s presentation of future life in ‘metaverse’ sparks fear, loathing, marvel and mockery

New York facing streets without cops because of COVID vaccine mandate

The Establishment Is Hiding Mass Resistance To Vaccine Mandates With The “Striketober” Farce